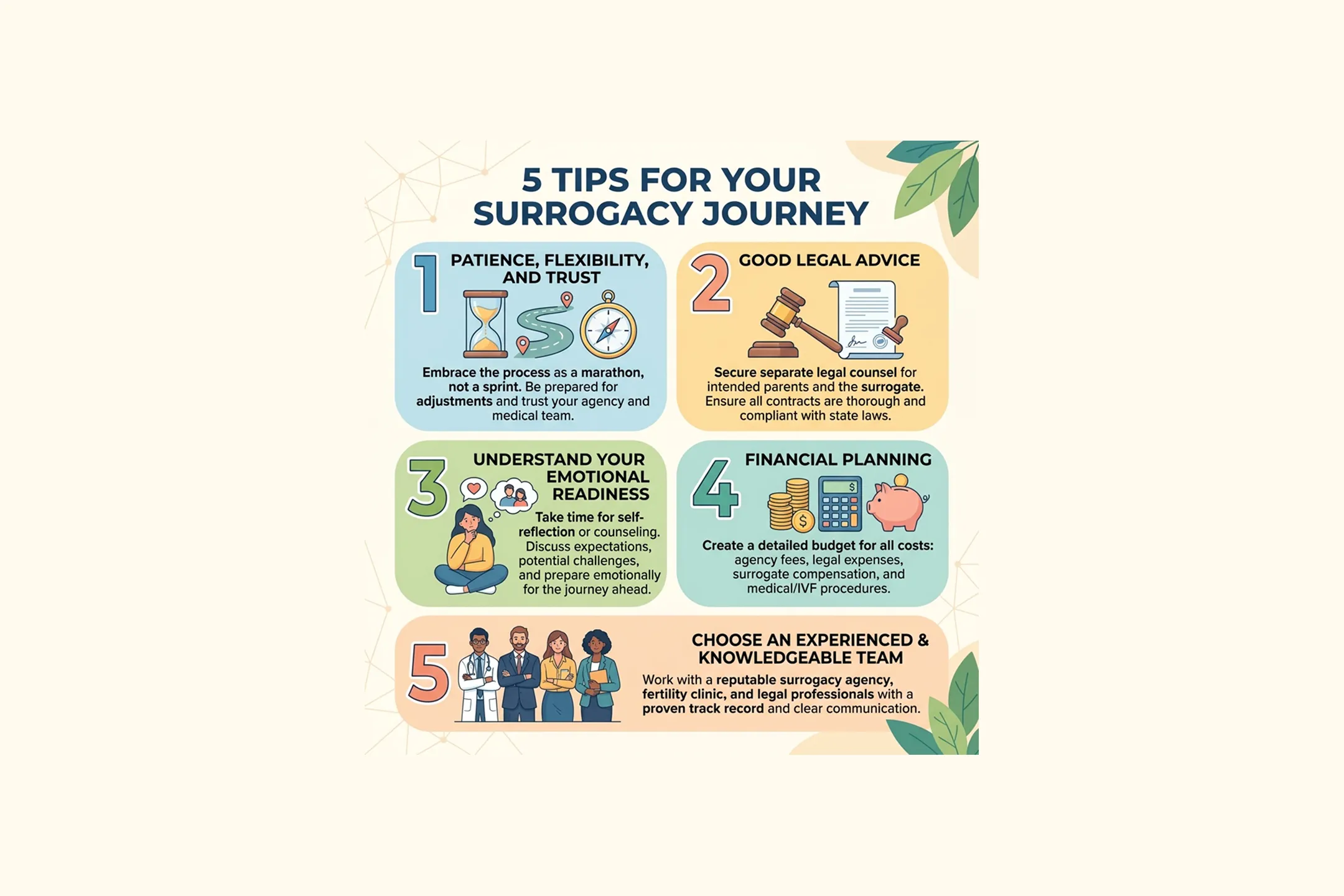

Every time I talk with prospective parents considering surrogacy, one of the main topics is medical insurance. The focus is generally on various options for maternity medical insurance and coverage for the newborn babies. The difference in cost between having medical insurance or not can be drastic.

Medical Insurance for Surrogates

Often, the gestational surrogate has medical insurance that covers maternity. It is important that a lawyer or insurance expert review the policy to see if there are any exclusions stating that the medical coverage will not cover a surrogate pregnancy.

If there is no exclusion, then the gestational surrogate may use her own insurance to cover the pregnancy and birth. If there is a surrogacy exclusion, then some other form of insurance must be procured to cover the pregnancy.

Surrogacy Medical Insurance & The Affordable Care Act (ACA)

One option for medical coverage for the gestational surrogate is an individual insurance policy. Under the Affordable Care Act (ACA) also known as "Obamacare," a woman may obtain medical insurance with maternity coverage for a monthly premium estimated at $400 to $500.

It is important to note that the Affordable Care Act mandates maternity coverage and newborn coverage. Therefore, a strong legal argument can be made that now, under federal law, no surrogacy exclusion is legal. However, it is not practical for Intended Parents to take on litigation to fight an insurance company that denies coverage. The cost of such litigation can be prohibitive and will just add another expense to an already costly process. In addition, the lawyer or professional may not guarantee insurance coverage.

The best that can be done is to review and understand the terms of the insurance as closely as possible so that an informed decision can be made as to whether to use the insurance and then to assess the level of risk of attempting to access the insurance.

Lloyd's of London Medical Insurance

In the event that the surrogate's insurance is in question, one possibility is to obtain policies underwritten by Lloyd's London.

One of the main brokers of this policy is The New Life Agency back-up plan (Lloyd's of London) for $3,000. Be aware, though, that the $3,000 is a nonrefundable payment to have the insurance available in the event of an insurance denial. If the policy must be utilized, these policies require a premium and further funding of a very high deductible that may range from $15,000 to $40,000, depending on the level of the plan, single or twin pregnancy, and other factors.

The benefit of the Lloyd's policy is that it is strictly for a surrogate pregnancy, so there is no chance of a loophole being used to deny coverage. The downside is the cost. The insurance will cover in the event of very high medical bills. For the most part, these policies amount to something like self-pay plans. The broker uses the deductible funds to pay medical bills. If the deductible is not fully used, funds are returned to the Intended Parents. If the funds are fully used, the policy of insurance kicks in to cover the unpaid bills.

Insurance & International Surrogacy

Another important factor to consider is that many Intended Parents come from countries outside of the United States. These international Intended Parents do not have their own insurance in the United States. Therefore, they must be concerned about how to insure their babies when they are born.

The most significant question is whether or not the babies are covered under the gestational surrogate's insurance policy. There are two schools of thought on this.

One side says that the surrogate's insurance should not be used because by contract and legal parentage order, the gestational surrogate is not the parent of the child. She, therefore, cannot place the baby on her insurance as a dependent.

The other side bases its answers on contract law. The insurance policy is essentially a contract. If the insurance contract provides for newborn care and the surrogate is adding a dependent, then this contractual provision will allow for coverage of the baby.

Also, in some jurisdictions, the parentage order can be done by post-birth order. With this procedure, the gestational surrogate is the legal parent of the child and therefore, she may put the baby on her insurance. By far, the best-case scenario is to secure an insurance policy that indicates coverage for a new baby as a contractual provision in the insurance contract.

All of these insurance matters must be discussed with your professional and legal team. They will be able to provide you with information and advice according to your specific circumstances and the coverage available with respect to your gestational surrogate.

Get the Latest Updates

Categories